Well, it’s been a month or so since the big move…am settled for now in National Park Village and the dogs are happy in their respective foster homes…

I’m sure she misses me…

…and him too @K9 Heaven in Auckland…

Just about everything is in storage and I’m slowly starting the big downsize…in the end I left a lot of stuff behind as I realised I didn’t really want or need it, nor the hassle of trying to unload it through Trademe or the buy and sell boards…

Looking pretty empty

Didn’t finish the final move until 4AM on the settlement day but by then I just wanted to be well shot of the place. No final pix as I accidentally packed my phone in one of the last loads…

National Park at night, walking home from work…

I’m liking living in the Village for now, being able to walk to and from work each day, meeting people, having occasional chats on the roadside, getting a feel for the Village vibe, not being last on the truck when the siren sounds…but…I miss the dogs and that’s my main motivation to find a new home.

Renting in the Village is not really an option as no one has heard of fences and dogs just run free, so it’s really a choice between buying an existing home or a block of land to put something on. The pickings are pretty slim in the Village, or even in Raurimu where we moved from but there are possibly some options in and around Owhango, although that would be the end of the walk to work thing…

Worse case scenario is opting to rehome Louie and Kala which opens up my own rehoming timeline but a a big cost…I’m away on course the next two weeks and will have to start sizing that option up on my return…

Thursday was the day for hearings into the granting of concessions (licenses) for commercial guiding operations on the Tongariro Alpine Crossing. These have potentially great implications for our small local business community, especially the smaller members. I had made a submission on the concessions and needed to be at the hearing to speak to my submission and hear the other speakers. Community stuff.

I was under the understanding that the final decision on the tender for my home would not be until the following day so felt secure heading away for the day.

At 11AM, just after the hearing started my lawyer messaged me to read my email. ANZ through its lawyers, Bell Gully, has given us til 3PM to accept another $2.5k in exchange for for a pre-Christmas settlement. ANZ has failed again and again to keep us informed on the progress of the forced sale of my home let alone any of the details. It has largely dumped this off on the young local real estate agent – to me, an act of total and abject cowardice on ANZ’s part.

Most else that I know of the process I learned from the tenderer.

It was difficult to make a decision when we didn’t know what the original settlement date was. Neither did Bell Gully (yes, really!). We discussed options and advised ANZ that we could beat the tender offer and that there was other interest in the property. We thought this other interest was really as they seemed comfortable with the $380k ballpark figure that Harcourts gave them.

Typically – in our experience – the Bell Gully letter was full of errors, no doubt due to the source of the information in ANZ.

(a) The Property was marketed for four weeks prior to the auction, and this has been followed by a further two week marketing campaign prior to the tender date. Since the auction, the agent contacted all previously interested parties to ensure they had the opportunity to submit a tender.

“…a further two week marketing campaign …” Not quite. The tender was not listed online until I had Harcourts head office on about the lack of marketing. Signage did not go up until halfway through the tender period. Prospective buyers making general inquiries about the district at Harcourts were not told of the property.

Following the marketing of the Property prior to the auction, Harcourts estimated the sale price of the Property would likely be between $250,000 and $280,000. ANZ also obtained a valuation from an independent registered valuer which put the forced sale range at between $262,500 and $300,000. The Tender price is within these ranges.

The tender price is conveniently at the bottom of ANZ’s assessed range. These figures beg the question “Why was Harcourts telling prospective buyer that the ballpark price for the property was $380k?”

ANZ’s reason for adopting the tender process was due to concerns that, in light of events leading up to the auction (including your client’s social media posts), proceeding with the auction at that time may not have resulted in the best sale price reasonably obtainable for the Property.

Blatantly false. If that statement held the slightest drop of water, why did ANZ wait until the morning of the auction, when people were already assembling for it, to cancel it? Surely it had nothing to lose in running the auction and then opting for a tender if the auction did not bring the result it wanted? ANZ was under no compulsion to accept any offer made in the auction and could have passed it in if it was not getting the bids it wanted. Certainly a tender was unlikely to achieve a better return than an auction.

Credit:Shutterstock / Patricia A. Phillips

The reference “…in light of events leading up to the auction…” can only refer to the questions asked by 1 News the previous day. Questions about it’s dirty laundry obviously make ANZ uncomfortable. Ditto for “…your client’s social media posts…” I checked regularly and was not informed of any adverse effects. Once again, it seems the only issue here is ANZ’s sensitivity to dirty washing and sunlight…

Potential purchasers have been nervous whether they will be able to get vacant possession of the property on the settlement date due to Mr O’Neill’s posts on social media.

Possibly however, again, this was not ever raised in regular checks with Harcourts. There were however discussions re my willingness to remain as a tenant.

There is a risk that buyers may begin to worry why the house is not selling if the sale is further delayed and moved to an 8 week campaign after the holiday period.

Right back at you, ANZ…surely this was the greater risk in the last-minute cancellation of the auction? That was hardly a confidence-engendering action, was it?

The location of the Property and its history have limited the number of buyers attracted to the Property.

“…The location…”? Situated on the volcanic plateau, five minutes drive from National Park Village, on the periphery of Tongariro National Park, directly overlooking the Raurimu Spiral Scenic reserve, twenty minutes drive from the biggest ski field in New Zealand and the one currently undergoing the biggest development in its history.

This location..?

“…its history…” For those who don’t know, here is ‘its history‘.- actually not much more than a piece of muck-raking from the NZ Herald. The truth is that, when this happened the house was barely ten years old…it has spent a greater period as a happy family homes with kids and dogs running around it…and goats and sheep and chickens…and the odd cat..

Further, we discussed ‘its history’ as part of the marketing plan. As that incident occurred over twenty years ago, the only reason that we decided to mention it was to cover any concerns arising not so much from the incident itself but the body of ignorance around it. But again, the reports from Harcourts were all positive, even though this was an issue that we were actively tracking…

The current Tender price may be “as good as it gets”.

Really…? When we said we would better the tender offer and when there had been other buyer interest in the property that had not been deterred by Harcourts’ $380k ‘value’… For perspective the rating value of the property is $425k..

So coming back to Thursday. It wasn’t til mid-afternoon that we were able to respond to the nonsense in ANZ’s latest – the 3PM deadline was never doable – but my lawyer was talking with them all afternoon.

Early that evening, my mortgage broker, ironically the same one who got us into this property in 2004, said she was confident i could get finance to beat the tender…

Not longer after, this arrived…

This is what getting screwed by ANZ looks like…

It really looks like ANZ was more focused on doing harm that ever realising a realistic return from this sale – it loses as well but that’s how spite works – obviously wanting to send a message about the true cost of standing up to its reckless lending and predatory conduct…It seems to have dead set on blocking an opportunity for me to buy the property back – where it still would have gained more than it got from the successful tender – than ever doing right by its shareholders and seeking the best possible result, which would have been the best result for all concerned…

…or, as we locals know it, the Tasman Sea, that large wild body of water that separates Australia from New Zealand. The big blue thing that keeps everything known to mankind that can kill you in Australia, and keeps New Zealand clean and green…

…except for banking where the process is reversed and the bad practices now being exposed by Rebecca Orr and the Australian Banking Royal Commission propagate across the Tasman into our fair land… Conversely, it would seem that remedial action, however slow, in Australia, doesn’t swim…

These principles are from ANZ’s 2017 Corporate Sustainability Review. It is largely focussed on ANZ operations in Australia but its scope includes ANZ New Zealand. Sadly, as you can see below, such initiatives by ANZ seem to be only limited to ANZ Australia – where is ANZ New Zealand’s Customer Fairness Advisor?

The former Australian Commonwealth Ombudsman, Colin Neave, was appointed as ANZ’s Customer Fairness Advisor. The Customer Fairness Advisor role is focussed on minimising reputational risk, and the risk of regulatory intervention, which may arise from:

• the retention or development of products which have an unfair impact on our retail and small business customers;

• shortcomings in the way in which we manage customers in financial difficulty and assess suitability for lending; and

• broader stakeholder concerns about the culture and values of large financial institutions.

During the year, Colin Neave developed customer remediation principles to assure our customers that ANZ will acknowledge and compensate for any failures quickly

ANZ corporate sustainability review 2017 p21

It’s not that bold a statement to suggest that ANZ New Zealand’s only awareness of the concept of reputational risk comes from the highly-critical Financial Markets Authority and Reserve Bank’s reports last month on banks’ culture and conduct in New Zealand. They are both worth a read: Culture and Conduct and Bank Incentive Structures.

ANZ New Zealand is:

a bank that loaned vast amounts to a borrower recovering from a serious head injury;

a bank that failed to determine if the loans were repayable. When I first found out about them in 2013, the accrued debt was just over $400k, with a company that had assets scarcely half that amount.

a bank that failed to to disclose this lending to me as the guarantor of that lending, even though by every standard of conduct, it should have.

a bank that, when challenged about this debt, lied about being authorised to disclose this information to me as the guarantor.

a bank that continued to lie by claiming that the Credit Contracts and Consumer Finance Act prevented that disclosure to me.

a bank that kept on lying when it made up information from the Code of Banking Practice to support its argument that disclosure obligations for guarantees and security are different. (they may be for some banks but for ANZ, by its own definitions, guarantees are part of security.)

a bank that, even when we said we could beat the sole tender offer and when there was other interest in the property, still accepted that single low tender offer.

So…ANZ New Zealand, where is your Customer Fairness Advisor? God knows you need one (at least)…

Once again the Office of the Banking Ombudsman strikes with all the power of the wettest of bus tickets…

All we can do is continue to push back…eventually the weak link will give way…

Thanks, Nicola

I am concerned that the best time-frame your “Early Resolution Team” can deliver is three months, more so when ANZ is already trying to forcibly sell my home now.

Further, for the record, your office did not respond to my last complaint. You did not comment on the evidence presented to you of:

– ANZ’s quite deliberate deception and obstruction, including the blatant fabrication of evidence.

– ANZ’s acceptance of guarantees as forms of security enabling its obligation of disclosure under the Code of Banking Practice.

– ANZ’s reckless lending and failure to ensure, under the Code, that the – borrower was reasonably able to repay the loaned amounts.

– ANZ’s statements that it did have an obligation of disclosure, especially where additional lending might cause the guarantor to reconsider giving the guarantee or where that lending was outside the purpose for which the guarantee was originally given.

Even when directed by the chair of the Banking Ombudsman Scheme to review this case, your office deliberately restricted that review to the process and not the issues raised.

You have attempted to deflect inquiries to government agencies like the Privacy Commission, Commerce Commission, etc but in each case, these government agencies have referred the matters raised back to you.

Unfortunately for the banking public of New Zealand, your office remains the primary watchdog against predatory bank practices. It beggars belief that even after the two reports released by the FMA and Reserve Bank on banking culture and conduct (Bank Incentive Structures, Bank Conduct and Culture, that your office remains on protecting offending banks from the consequences of their poor conduct. It is the failure of the Banking Ombudsman Scheme that has allowed banks in New Zealand to take advantage of the vulnerable and disadvantaged.

Tenders for my home closed on Friday night and, as I understand it, there was only one response and that was a very low offer i.e. less than the adjacent property that sold a couple of months ago but which is not much more than four hectares of blackberry and a small totally non-compliant residence – compared to a fully compliant three-bedroom home, with a large garage, sleep-out, and sealed driveway on thee hectares of regenerating native bush…

Pretty much what we expected. ANZ is terrified of media coverage exposing its reckless lending and the deceptions it employed to cover it up. In a desperate attempt to shield the forced sale of my home from such attention, it cancelled the well-subscribed auction on 8 November in favour of a less favourable tender process. Many buyers who will happily bid at an auction will not submit a tender proposal because they see it – rightly – as carrying more risk than an auction.

ANZ can accept this low offer – and lose even more. It could reschedule the auction it so untidily cancelled on 8 November – after a suitable period of remarketing. It could accept that this is not going to get any better, cut its losses and make right the damage that it has dome over the last fourteen years…

So, here we are ANZ, Plan B worked no better than Plan A. Your sole response won’t come anywhere close to the amount of money that you are demanding as a result of your unchecked and reckless lending processes, your total and blatant disregard for the obligations placed on you by the Code of Banking Practice.

Maybe it’s finally time to do the right thing, to cut your losses and make good the damage you have done…?

In other news, thank you to every one who called or messaged to give the Banking Ombudsman a nudge on Friday. I think that we can safely say that the message was received. While the Banking Ombudsman was too busy to make a simple call to ANZ to query its tender process under its fair, reasonable, ethical and consistent obligations in the Code, she did find the time to call me twice, and then my lawyer to complain about it.

Unfortunately this is a bed entirely of her own making. If you are going to be a watch dog, you need to be able to bark, not whimper and wag your tail. An agent of the Office of the Banking Ombudsman should enter a bank to the tune of the Imperial March not Here Comes the Sun.

I have been to the Banking Ombudsman three times: 2014, 2016 and 2018…and each time been totally underwhelmed:

Where we provided a legal opinion that ANZ erred in not informed me of the additional lending, the Banking Ombudsman did not explore this further because ANZ disagreed.

Where we requested a review of my case through the chair of the board of the Banking Ombudsman, the QC appointed to that review was specifically constrained to only consider the process followed and NOT the issues raised.

Where we provided evidence of quite blatant obstruction and deception on the part of ANZ New Zealand, the Banking Ombudsman was silent.

ANZ has an obligation under the Code to ensure that any body borrowing money from it is reasonably capable of repaying the loaned amount plus agreed interest. ANZ did not do that with this lending. The Banking Ombudsman would not comment..

The Banking Ombudsman attempted to deflect complaints to government agencies like the FMA, Privacy Commission, Commerce Commission etc. Each agency has responded that it considers the Office of the Banking Ombudsman to be the most appropriate agency for investigation and resolution of these and similar issues. While I tend to agree with the Banking Ombudsman’s logic on this, the Government, at this time, does not.

ANZ has desperately clung to the Banking Ombudsman’s findings as its sole defence against my challenges. Sometimes we wonder if anyone at ANZ has actually read those findings in the context of the actual complaints and whether its “the Banking Ombudsman says” mantra has always worked in the past to keep the light at bay…

Sooner or later, the Banking Ombudsman will need to review her position on these issues. They will not bear up under the light of increasingly public scrutiny…

Damned if you do, damned if you don’t…maybe the Banking Ombudsman is in a limbo similar to my own at the moment…

ANZ New Zealand is being offered every opportunity to do the right thing…my lawyer has been busy over the last couple of days…sent to ANZ this morning via Bell BGully…

ANZ is now so shy of adverse media it will seek a less profitable outcome to try to keep its dirty laundry under cover…

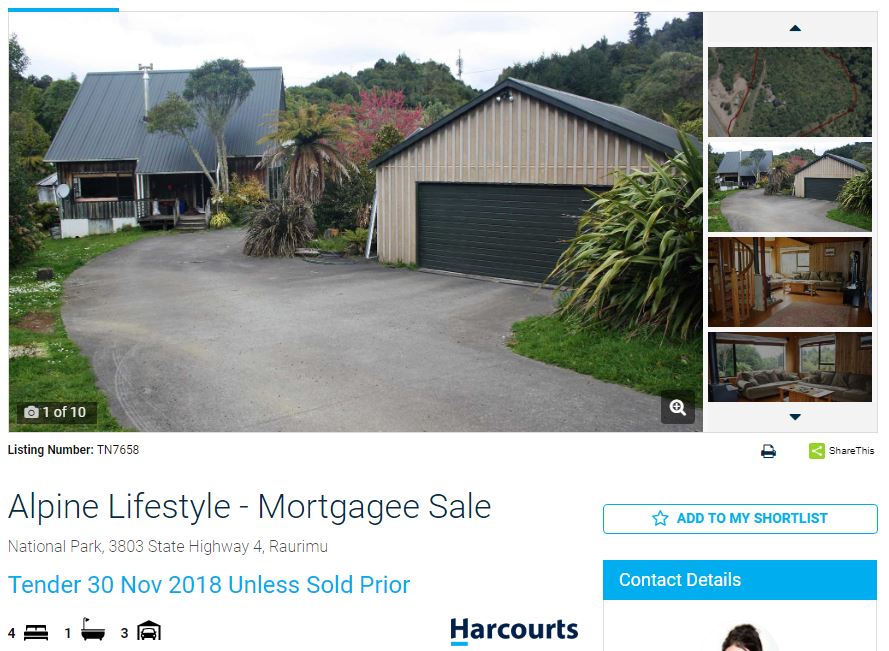

From this…

Mr O’Neill’s home, situated at 3803 State Highway 4, Raurimu (“the property”) was scheduled to be auctioned by ANZ New Zealand (“ANZ”) at 11.00am on 8 November. My client instructs that there was considerable legitimate interest in this auction.

However, our client instructs that the ANZ cancelled the auction at the last minute when prospective buyers were already assembling at the auction location. The ANZ has given no reason to my client for this last minute action; and I understand that this may have been a reactive response to questions asked by the media with regards to the sale.

The ANZ has not communicated with Mr O’Neill at all. On 15 November 2018, an agent from Harcourts advised him that because he “had a right to know’ the ANZ had instructed that the property was to be sold by tender. Tenders are due by 4.00pm on 30 November 2018.

My client instructs that two days later, noting the short duration of the tender, he was concerned that an online listing had not been posted immediately and raised this concern with Harcourts head office. A listing appeared early the following week; however, signage on the property was not erected until later that week. There has been no contact with Mr O’Neill to arrange viewing opportunities and/or further open homes for interested purchasers. Mr O’Neill instructs that he has cooperated fully with previous open homes.

…to this…really…?

Mr O‘Neill believes, and certainly there appears to be no evidence to refute this belief, that the ANZ did not intend for him to learn of the tender until it had closed.

The notice period for this change in tactic is of concern, as my client does not consider that this approach will result in an appropriate response being obtained from the market. Also, as mortgagor he may suffer considerable loss because of the approach taken by the ANZ, particularly, at this time of year; and after having cancelled the auction process that promised the best result for all parties concerned.

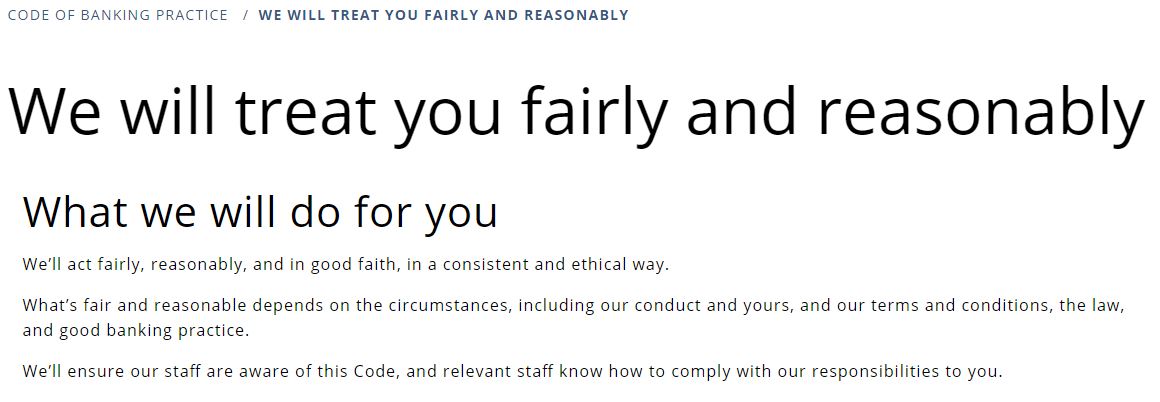

It is of concern that there appears to be an ongoing failure by the ANZ to communicate with Mr O’Neill either directly or through me. My client is of the view that the switch from an auction to a tender process by the ANZ is potentially a less effective form of marketing. It would also appear that as the ANZ stands to recover less of the debt via tender process, it could be viewed that this action is solely intended to protect the ANZ from unwanted media interest. If that is the case, then the approach could be considered reprehensible and inconsistent with the obligation the ANZ has under the Code of Banking Practice to “act fairy, reasonably, and in good faith, in a consistent and ethical way’.

My client views the situation for ANZ as being entirely of its own making, which includes its reckless lending; and in its conduct since he first raised his concerns five years ago. If the growing media and political interest is uncomfortable for ANZ, then this is unfortunate; however, Mr O’Neill should not be disadvantaged as a result. I would also draw your attention to the effects upon Mr O’Neill’s physical and psychological well-being, which is resultant from the conduct of the ANZ towards him.

Without conceding our client’s position in this matter, our client considers that an appropriate response is an 8 week campaign for a tender after the Christmas period. Alternatively, our client’s offer to facilitate a resolution remains open.

On 5 November the Financial Markets Authority and the Reserve Bank released their joint report into bank conduct and culture in New Zealand On 15 November they released another report into bank incentive structures.Both reports are highly critical of banks’ conduct in New Zealand, find most if not all wanting in terms of their culture and conduct; measures in place to mitigate poor conduct; and the responsibilities of senior bank officers and of boards.

While everyone seems to accept the findings of the reports, no one yet seems to want to ask the questions around making it right. ANZ New Zealand posted a profit of $1.99 billion in the last twelve months, that’s around $5.4 million dollars a day – profit! Should ANZ be required to allocate a proportion of its profits to making it right for the New Zealander who, to be blunt about it,have been screwed by the greed of ANZ and other banks? ANZ was quite happy to incentivise and pressure its staff into making sales that should never have proceeded and now it needs to make this right.

In 2004, I guaranteed my partner’s company for a house for our daughter when we moved away. That property was sold in 2005 and I thought nothing more of it. At the same time my partner was recovering from a serious head injury. When she was working her income was less than $50k a year and income from her company was limited, less than $10k a year. Still ANZ, from 2005-2009, extended credit to her that, by the time I found out about it at the end of 2013, had accrued to $408k. I don’t believe that she is responsible for her actions in this period. If I did, then I would be taking the appropriate actions.

When I challenged ANZ over this, it said that it had no authority to discuss this with me. That was not true: the loan documents include a specific clause enabling disclosure to guarantors and the Privacy Commissioner also ruled in 2012 that this sort of information can be considered personal information for the guarantor.

ANZ said that the Credit Contracts and Consumer Finance Act (CCCFA) prevented it disclosing this information.Again, this is untrue: this Act only applies to personal lending and does not mention company lending at all.

To support its position that guarantees are treated differently that security, ANZ then made up information that it attributed to the Code of Banking Practice. Even if that Code did say that, ANZ’s guarantee and loan documents clearly define security as including guarantees.

Under the Code of Banking Practice, ANZ has an obligation to only extend credit if it is satisfied that the person borrowing the money can reasonably pay it back. Under the same Code it also has an obligation to tell people who have offered guarantees and other security of new or additional lending against that guarantee or other forms of security.

The Code also includes a general obligation for banks to act fairly, reasonably, ethically and consistently. While we might agree that they are consistent in their conduct towards customers, the recent reports from the FMA and Reserve Bank find that ANZ et al fall short in acting fairly, ethically and reasonably. Who will hold them to account for their actions?

The reports find the regulatory frameworks in New Zealand for banking are weak. In part this may be due to gaps in legislation and culture of ‘not our problem’ – have a look and see how many government agencies with a regulatory output have more content on their websites about what they don’t do versus what they actually do. From my experience with these agencies, this is largely due to inadequate leadership and an unwillingness to get into the fight. Nowhere is this more apparent that within the Office of the Banking Ombudsman. Although not part of Government – something I hope you will consider changing – this office should be the primary watchdog to safeguard ordinary New Zealanders against predatory banks like ANZ.

In November 2016, I submitted a detail complaint (attached) with supporting documentation to Office of the Banking Ombudsman which initially rejected it out of hand. After three months, it produced a single page response (attached) that did not address any of the issues raised. Acting on advice from the Office of the (real) Ombudsman this year, I submitted a complaint to the chair of the Board of the Banking Ombudsman. Although she did appoint a QC to review my case, he was specifically limited to only review the process applied by the Banking Ombudsman and not the actual issues raised.

ANZ was scheduled to forcibly auction my home on 8 November.I cooperated fully with the real estate agent as, if the sale proceeded, it was in my best interests as much as ANZ’s for the auction to achieve the best possible result. That auction was cancelled an hour before it was due to proceed. I believe that ANZ did this to prevent 1 News screening a story on the auction that night. ANZ did not communicate with me at any time to advice of the cancellation, the reasons for the cancellation or what would be happening next. A week later, the real estate agent called me in tears after she had found out my home was instead to be sold by auction. I don’t believe that I was meant to know about this til it was a done deal. That tender closes 4PM Friday 30 November.

There is probably not much that can be done to deter ANZ from its course this time. Like most bullies, the only things that put it off are a good hard punch to the nose, or being publicly embarrassed. To that end, if you would like to help, please do not go off and punch a banker. Instead, you might wish to ask the Banking Ombudsman or ANZ if they would like to offer some comment on the issues raised in the attached complaint (sorry, it is a bit chunky as there are a lot of issues) or ANZ’s conduct since I first challenged it in 2013 (yes, five years ago) and over its conduct of the tender.

Contacts for the Banking Ombudsman are Nicola Sladden nicola.sladden@bankomb.org.nzor for the chair of the Board, Miriam Dean miriam.dean@barrists.co.nz. Unfortunately I do not have any direct contacts with ANZ other than to direct you towards its totally inappropriately named Customer Financial Well-being Unit.

Longer term, please consider how best predatory corporates like ANZ New Zealand can be held accountable and required to make good, as best they can, the damage their greed has done to so many ordinary New Zealanders.

My suggestions are that we

bring the Office of the Banking Ombudsman in as an arm of Government;

ensure that other regulatory agencies like the FMA and Commerce Commission are both empowered and energised to pursue errant corporates; and, most of all,

establish a Royal Commission to peel off the scab of banking in New Zealand. I do not believe for one second that the Tasman Sea is a barrier adequate to protect us from the behaviours now being exposed by the Australian Banking Royal Commission.

Throughout ANZ New Zealand has relied on the Banking Ombudsman as the linch-pin of its defence. It really needs a better linch-pin. The Banking Ombudsman (Nicola Sladden nicola.sladden@bankomb.org.nz) and the Chair of the Banking Ombudsman board (Miriam Dean miriam.dean@barrists.co.nz) have consistently avoided the issues at the core of this dispute.

Nicola Sladden nicola.sladden@bankomb.org.nz

All off the record, of course, like anything is ever really off the record, but I understand that some of Nicola’s responses to media inquiries have not been consistent with her formal findings in this case. Once the weak link goes…

Miriam Dean miriam.dean@barrists.co.nz

These are the questions that Miriam and Nicola do not want to answer and that should be put to them:

Question 1

ANZ New Zealand’s guarantee and loan documents include guarantees as forms of security. The Code of Banking Practice (until the May 2018 version) says that banks have to provide any party providing security of the details of any lending against that security. This includes

the annual interest rate and whether it may be changed during the period of the credit facility;

all fees and charges (including government charges and taxes);

the period for which the credit facility is available;

the repayment terms, including any terms relating to early repayment costs.

If banks take the Code of Banking Practice seriously – and it’s the Banking Ombudsman’s job to make sure that they do – why didn’t ANZ tell me about all the extra lending to my ex-wife’s company?

Question 2

Why was the Banking Ombudsman not concerned when:

ANZ New Zealand said that it had no authority to disclose information to me – when it did have that authority and a previous determination by the Privacy Commissioner also said that it should disclose this information.

ANZ New Zealand said that the Credit Contracts and Consumer Finance Act 2003 prevented disclosure to me. The truth is that this Act, by definition, only covers personal lending and does not even mention company lending.

ANZ New Zealand made up information that it attributed to the Code of Banking Practice to support its position that it did not have to disclose details of additional lending to guarantors.

Question 3

The Code says that ANZ New Zealand can only provide credit or increase credit limits when the information available to it leads it to believe the customer will be able to meet the terms of the credit facility (that means, repay the loan). The Banking Ombudsman has held banks accountable under this obligation in its case notes.

Why didn’t the Banking Ombudsman consider this obligation when ANZ loaned hundreds of thousands of dollars to a small company with a weekly income of less than $200 (that’s what ANZ New Zealand CEO Dave earns in about 8 1/2 minutes)?

Question 4

The Code requires banks to act fairly and reasonably, in a consistent and ethical way.

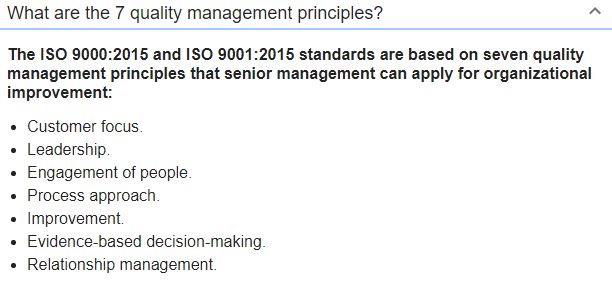

Nicola and Miriam, could you please tell us how ANZ New Zealand’s conduct in this issue could ever be considered fair, reasonable or ethical? Yes, we might give ANZ New Zealand points for consistency but that’s not always a good thing. ISO 9001 just means you can do things badly all the time…

…and just as an aside, I think we can give ANZ New Zealand a great big ‘F for Fantastic‘ on each of those seven principles…

For many of us, “Cover me!!” means we’re about to do something that may not turn out well…not so much a military “Hold My Beer!” as this needs doing and I’m going to need to some help… Covering fire is a little more personal than the good old ‘Fire mission, Regiment’ and other such methods of registering one’s unhappiness with a given individual, object or grid square…

But there’s other ways of providing cover…

Be honest, you all had a snigger when you saw this one, like, der, man…

It would be nice to think that it would be possible to deter ANZ New Zealand with a massive show (or application – I was, after all, the Force Application lead for most of my four years in the Air Force) of force/might/power. Even it such force/might/power was available, poor old ANZ New Zealand is like a mega-dinosaur controlled by a myriad of different brains that don’t talk to each other that well, if at all…any effect registered by one is unlikely to affect the others…

With ANZ New Zealand, the only brain that counts is its ego, the bit that gets worried when it might look bad; the one whose worst nightmare is a world where all its bribes of super-low interest rates (coincidentally announced just after the release of the FMA/RBNZ report on banks’ conduct in New Zealand) or the millions of look-good dollars that it invests into sports… Like the cool kids at school, looking bad is what ANZ New Zealand fears the most…it cancelled the auction of my home to prevent 1 News running the story on it…

The path to ANZ New Zealand’s main ego brain is indirect…for any direct approach to work the brain would have to care and the simple truth is that ANZ New Zealand doesn’t care what you say to it, because ‘the people’ are beneath it, beneath the executive team, beneath the board, beneath the CEO who ‘earns more in an hour’ than most Kiwis take home in a week…instead the path to ANZ New Zealand’s care factor is external and three-fold:

The political realm, especially those elected representatives who have been supportive to date. They have been looking at the changes necessary to close off all the remaining loopholes relating to banks’ lending.

The media who play a canny game of what to release when…

to be continued…(nothing worse that a looooong post….)

It’s actually not about covering me…it’s about covering each other…

It probably wasn’t appropriate that I go away for a three day conference in Wellington, not when I should be at home doing everything in my power to fend of ANZ’s latest attack.

Have cancelled the auction – which it still hasn’t told me about or advised the reasons for – ANZ then opted for a quiet tender sale which I only heard of from the local agent. I think that ANZ was hoping that it could slip this up the radar where no one would notice til it was a done deal…so much for this…

No listing was posted on Friday and I did not check over the weekend but this was up this morning:

Strangely, noting ANZ’s previous insistence that there be a sign on the front gate, there is no sign this time round (not yet anyway)…another sign of ANZ’s intention to keep this latest dirty work as quiet as possible…

Just to be clear,although I fought to halt the auction that fight was against the whole forced sale process and the false premise that it was based on…I cooperated fully for the advertising open homes prior to the auction as it was obviously in everyone’s best interests for the auction – if it proceeded – to realise the best return possible…

The tender sale that ANZ has now opted for does not have the same potential as it is not marketed as broadly, lacks the option for viewing or open homes (no inquiries have been made by ANZ or Harcourts about this), and will not have the same potentially competitive environment of a good auction…It also hasn’t been listed oin Trademe this time, further reducing the coverage and likely return…

Our conference hours were quite civilised at there was an opportunity to wander around the capital. Obviously all this with ANZ was never far from my mind and I could not help note an ironic imagery between some of its facilities and pop culture…

Is that me? Standing before the Dark Tower? Challenging the giant…?

That’s how it has felt for so long as I kept all this inside. Not just out of Kiwi staunchness – yes, admittedly a factor – but also because it has been clear from the start that ANZ’s best option, once its poor conduct was exposed, settling quietly was in everyone’s best interests…

Mike King was the keynote speaker on Saturday – anyone who has not been to one of Mike’s Key to Life addresses should go or at least make sure that their children do…

Mike’s themes is that one of the biggest obstacles to opening up and sharing our problems is that we don;’t want to admit to vulnerability or failure coz Kiwis don’t do either…

Not wanting to admit or share that I wasn’t top of the world was the other reason that I kept this close for so long…that’s dumb because once I put it out there, I have been overwhelmed by the support and advice and just-being-thereness from all the communities I am a part of…